|

|

Ser GEÓLOGO é:

Ver, antecipar e evitar prejuízos causados por fenômenos naturais

|

|

Você é o que você sabe. Fique bem informado usando o

Portal do Geólogo, o melhor e mais atualizado site de Geologia, Ciências

da Terra e de Mineração no Brasil.

|

|

|

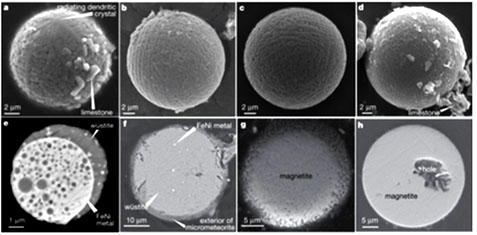

Como reconhecer um meteorito?

Após a queda do meteorito em Santa Filomena o Brasil é sacudido por uma onda de questionamentos. Parece que todo o cidadão tem um "pedra", escura, pesada e misteriosa, que parece ser um meteorito.

Consequentemente a minha caixa de emails, todos os dias, transborda com perguntas e mais perguntas sobre rochas que "caíram do céu".

Cada email vem repleto de fotos das mais diversas rochas e, a maioria, você deve ter adivinhado, está longe de ser um meteorito. São milhares de emails recebidos o que demonstra o enorme interesse.

Se você quer saber mais sobre o tema recomendo a leitura do texto abaixo. Ele trata, de uma forma simples e objetiva como você poderá reconhecer um meteorito.

|

A quarentena mata. Um exemplo do que está ocorrendo no Brasil.

O exemplo que vou contar mostra o que está ocorrendo no Brasil que não é contado pela mídia.

Todos sabem que um dos produtos mais fundamentais na luta contra as mortes do Covid-19 são os respiradores/ventiladores. Sem eles as pessoas morrem nos leitos de UTI miseravelmente, sem poder respirar....clique para ver mais.

|

Água no Brasil

Somos um país riquíssimo e a água é um dos nossos maiores bens.

Muitos brasileiros não têm ideia do que significa ter água de qualidade, de fácil acesso, sem necessidade de tratamentos caros. Veja aqui tudo sobre a água.

|

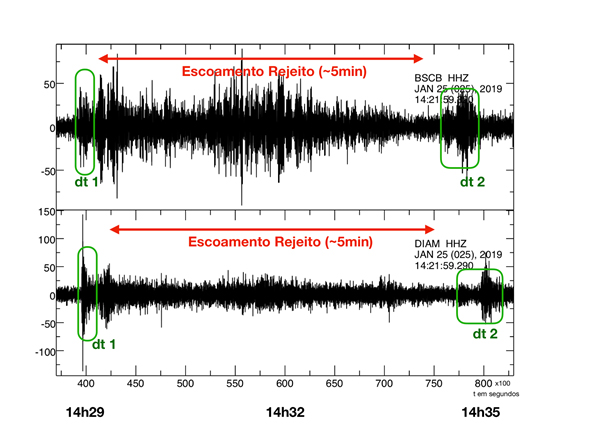

A verdade sobre as explosões da Mina do Feijão em Brumadinho

No dia 25 de Janeiro de 2019 a barragem de rejeitos da Mina do Córrego do Feijão rompeu.

A gigantesca massa de rochas e lama se deslocou a uma velocidade assustadora matando tudo e todos que estavam no seu caminho.

Foi o maior desastre da história da mineração brasileira. Maior ainda do que outro, similar, causado pela mesma empresa, a VALE, três anos antes, em Mariana.

|

Água, será verdade que a água do mundo está acabando?

Vivemos, hoje, uma gigantesca histeria coletiva fomentada pela mídia mundial.

Esta mídia propaga, sem restrições, que em breve faltará água no Planeta Terra — um futuro sombrio e atemorizante.

Segundo esses noticiários:

-Teremos que parar de produzir eletricidade a partir de hidrelétricas.

-A produção de alimentos, em plantações irrigadas, irá cessar.

-Centenas de milhões de pessoas, como zumbis, vagarão pela superfície da Terra em busca de um pouco de água — matando se for preciso.

-Em poucas décadas, estaremos vivendo um clima apocalíptico digno de um filme de Mad Max — a confusão e a desgraça imperarão.

Será tudo isso verdade?

|

NÃO SEJA UM ALVO – PROTEJA-SE!

Algum dia você já se perguntou se o seus dispositivos de comunicação, computador, laptop, celular etc... foram invadidos e alguém está espionando os seus passos, seus segredos, copiando, fotografando e a tudo gravando?

NÃO SEJA UM ALVO – PROTEJA-SE!

O seu Manual de Sobrevivência no Mundo Digital

|

A história não contada de NOVO PROGRESSO - uma história da Geologia

Algum tempo atrás, trabalhando como geólogo na Amazônia vivi uma aventura completamente inusitada.

É uma coisa que só a geologia proporciona.

Em decorrência desta experiência foi criado um novo município — NOVO PROGRESSO — no meio do Tapajós, no Estado do Pará.

Hoje, resolvi contar esta história, em um pequeno livro que lanço, em primeira mão, na Amazon.com.br

|

A maior descoberta arqueológica da década

Você sabia que há milhares de anos um grupo de paleoíndios, desconhecido, fez as maiores obras de aquicultura da história da humanidade — no interior da Amazônia?

Abra a sua mente.

Com o avanço do desmatamento e com o auxílio da filtragem digital em imagens de satélites, descobri nada menos do que 1.200 belíssimas construções milenares, no meio da Amazônia — totalmente inéditas.

São obras pré-históricas, algumas datadas em 6.000 anos, incrivelmente complexas e avançadas.

Neste livro você se surpreenderá com essas construções monumentais, grandiosas e únicas, feitas por aqueles que foram os primeiros arquitetos e engenheiros do Brasil.

Participará de uma importante descoberta arqueológica que vai valorizar um povo sem nome e sem história. Um povo relegado a um plano inferior e menosprezado pela maioria dos cientistas e pesquisadores.

|

A Vale mente

Vídeo mostra que no momento da ruptura da barragem do Feijão existia uma operação em andamento.

Em torno de 20 funcionários, que trabalhavam no dique da barragem, são mortos. Poucos sobreviveram.

Isso ocorreu em uma barragem que a Vale dizia estar sem atividades.

A Vale mentiu, mais uma vez.

As consequências virão.

|

A Mineração Depois de Brumadinho

Em 2014 o nosso mundo ruiu: veio a Dilma, o Lobão a ganância e a corrupção.

Em poucos anos o descaso e a incompetência governamental afastou os

investidores. Fomos arrasados pelo desemprego e o setor mergulhou em uma crise

nunca vista.

Agora, quando estamos mais uma vez, tentando emergir deste longo inverno com a

promessa do retorno dos investimentos e de importantes mudanças favoráveis ao

setor mineral, o nosso mundo, mais uma vez, entra em colapso.

E você sabe quem é a responsável por mais essa gigantesca catástrofe?

A maior mineradora do Brasil e uma das maiores do mundo — A Vale.

|

O Mistério de Brumadinho

Como uma barragem de rejeitos, abandonada, seca e estabilizada se rompe causando uma onda arrasadora de lama que mata e destrói?

O que causou essa instabilidade?

De onde veio a água necessária para liquefazer o rejeito?

Por que as inspeções feitas poucos meses atrás não constataram o perigo iminente?

A mineradora Vale estava reprocessando os rejeitos na época do rompimento?

|

|

|

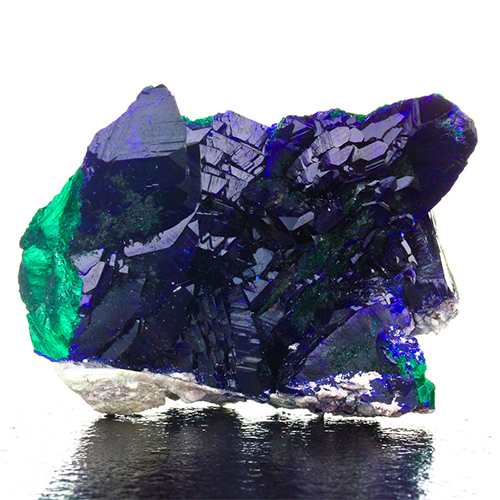

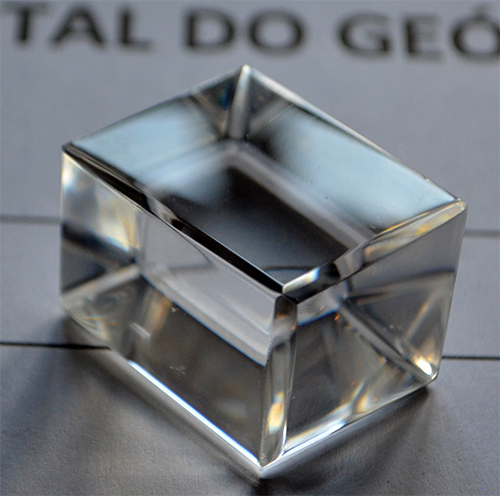

Iceland Spar a pedra que descobriu as Américas

Iceland spar é uma das gemas mais extraordinárias e belas que um colecionador ou estudioso pode encontrar.

O nome Iceland spar, ou espato da Islândia é, também, sinônimo de calcita ótica. Esta gema preciosa se caracteriza por sua incrível qualidade, total transparência e quase ausência de imperfeições, impurezas e de cor.

|

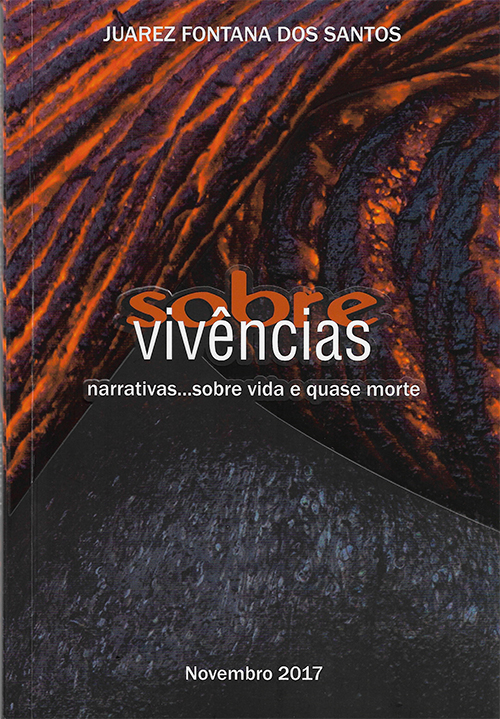

Sobrevivências

Juarez Fontana é um geólogo gaúcho, com mais de 50 anos de carreira, que resolveu contar um pouco de suas extraordinárias experiências.

Embarque nesta viagem e conheça um pouco do colorido mundo que só os geólogos vivenciam.

|

O aquecimento global e a ignorância humana

O aquecimento global é um fenômeno natural que se repete há milhões de anos e vai continuar a ocorrer com ou sem a nossa presença.

Nós não somos os responsáveis por esse ciclo de aquecimento global que começou muito antes da poluição causada pelo Homem.

A nossa poluição, fruto da irresponsabilidade de muitos, é, apenas, um fator adicional nesta equação do aquecimento-resfriamento Global.

Mesmo não sendo a principal responsável a poluição do ar, das águas e da terra é um crime contra a humanidade e como tal deve ser tratado.

|

|

|

Geologia é vida!

Os geólogos, são os olhos e os ouvidos da natureza, pois eles têm a incrível capacidade de entender e traduzir esta linguagem espetacular.

Geólogo: parabéns pelo teu dia!

|

A descoberta do estanho de Pedra Branca, Nova Roma,GO

A descoberta do estanho de Pedra Branca, Nova Roma/GO

O meu reconhecimento aos amigos de uma equipe vencedora, cujo trabalho e criatividade alimentou e empregou dezenas de milhares de pessoas por quase uma década.

E o meu respeito àqueles empregados, sinônimos de integridade, que optaram pela pobreza não usufruindo dos seus conhecimentos para benefício próprio.

|

|

|

|

|

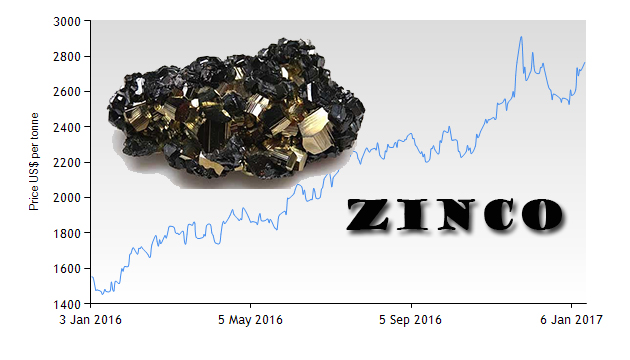

Mineração: as melhores apostas de 2016

O ano de 2016, mesmo começando “mal das pernas” acabou sendo, simplesmente excelente, para a indústria da mineração,

em especial para as commodities metálicas que, em média, deram retornos acima de 200% para os investidores...

|

|

|

|

|

|

|

|

|

O perigo dos deslizamentos de terra

Sempre nas épocas das chuvas os escorregamentos em áreas urbanas com forte declividade são responsáveis por inúmeras tragédias. A grande ironia é que todos esses dramas e suas danosas consequências são, quase sempre, totalmente previsíveis e, portanto, evitáveis.

Veja neste artigo, se você a sua família ou o seu prédio estão em perigo.

|

Somos, realmente responsáveis pelo aquecimento global?

É incrível como as pessoas e entidades desconhecem o fato de que os aquecimentos globais e resfriamentos globais vem se repetindo no tempo geológico,

nos últimos milhões de anos, sem nenhuma influência do ser humano. Culpar o Homem, unicamente, por este ciclo de aquecimento global que já perdura há mais de 11.000 anos é um erro grave.

|

A lenta morte da pesquisa mineral...

A história está cheia de exemplos onde esperar simplesmente, sem reagir, é sinônimo de catástrofe.

Aqui no Brasil estamos vendo o governo prometer um novo Código da Mineração, há anos.

E nós, pacientemente, aguardamos.

Alguém aí se lembra do Código da Mineração, ou do Marco Regulatório da Mineração???

Infelizmente a maioria dos geólogos e mineradores devem se lembrar. Afinal a maioria perdeu o emprego e viu as empresas de pesquisa mineral quebrarem e fugir do Brasil em um desastre gigantesco que parece ainda não ter terminado.

Em 2014, nós do Portal do Geólogo já alertávamos sobre o que vinha pela frente...veja que nada mudou.

|

Exploração mineral: um país sem memória

Você sabe onde está guardado o gigantesco acervo coletado pelas centenas de empresas de mineração, que investiram bilhões ao longo de décadas em pesquisa mineral no Brasil?

http://www.geologo.com.br/semMemoria.jpg

|

Seis Lagos o eldorado que não se concretizou

Sei que você já deve estar cansado de ler e ouvir falar sobre o nióbio e sobre uma teoria da conspiração propagada, frequentemente, na mídia. Sei, também, que você deve se perguntar se tudo isso é verdade.

Será que o nióbio sozinho pode levar o Brasil e seu PIB aos píncaros da glória como o falecido Enéas Carneiro e muitos falam e escrevem?

|

A ameaça de Pasadena: a vez e a hora de Dilma Roussef

Em 2006, quando Dilma Roussef era a Presidente do Conselho de Administração da Petrobras, foi concretizada a compra da Refinaria de Pasadena, no Texas.

Estava efetuado o primeiro grande rombo da Petrobras: um marco histórico da corrupção brasileira moderna cujos desdobramentos só poderiam ser intuídos 10 anos depois...

|

|

|

|

|

Spinifex: a textura que mudou a economia da Austrália

Uma descoberta interessante que mudou os rumos da indústria do níquel no mundo...

|

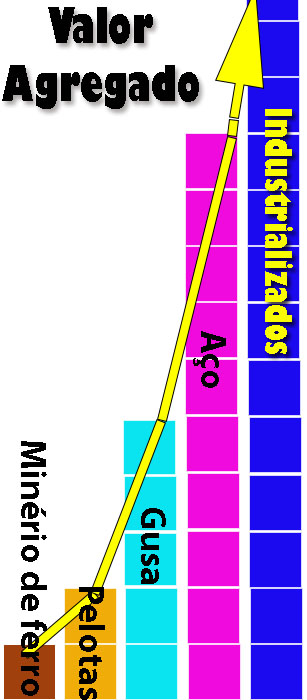

Adicionar valor ou morrer tentando

Durante décadas a maioria dos mineradores do mundo, incluindo as gigantes Vale, Rio Tinto e BHP, se restringiram a produzir minério com o menor valor agregado possível.

Quanto muito elas produziam concentrados, deixando para as metalúrgicas o trabalho do refino e da produção de produtos mais elaborados e, obviamente, muito mais caros.

|

|

|

Mineração & Brasil: o país do futuro?

A BMI Research, uma empresa do Grupo Fitch, na sua análise macroeconômica, diz de forma objetiva, que o Brasil será a grande aposta no futuro próximo...

Se eles estiverem corretos veremos uma revolução na mineração brasileira, com a volta dos investidores.

|

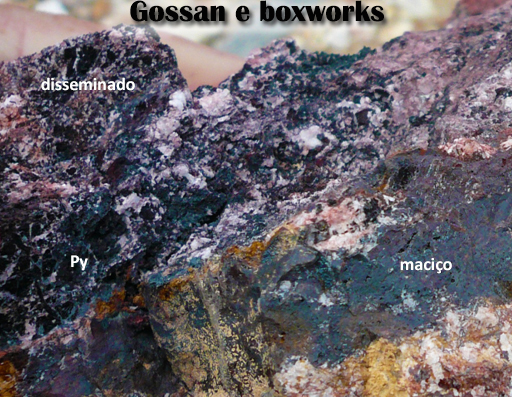

Você conhece um gossan?

Foi através da descoberta de gossans na superfície que foram descobertas a maioria das jazidas de níquel sulfetado tipo Kambalda na Austrália na década de 60 e 70.

Nesta época, a capacidade do Geólogo de distinguir entre gossans derivados de sulfetos de Cu-Ni dos derivados de sulfetos estéreis como a pirita e pirrotita foi o diferencial entre os bem sucedidos e os losers.

|

|

|

|

|

|

|

|

|

Mineração: quem vai tapar os buracos amanhã?

Um dos fantasmas mais assustadores da mineração mundial é o day after, quando a jazida está completamente exaurida e a empresa para de produzir. A partir deste momento, se não houver um bom planejamento, todos perdem...

|

Exploração mineral: um país sem memória

Você sabe onde está guardado o gigantesco acervo coletado pelas centenas de empresas de mineração, que investiram bilhões ao longo de décadas em pesquisa mineral no Brasil?

Surpreenda-se!

|

|

|

Mineração: adicionar valor ou morrer tentando...

Por gerações as mineradoras venderam bilhões de toneladas de um produto moído, baratíssimo, quase sem nenhum valor agregado, que era transformado nos países importadores como a China, Japão e Coréia em carros, eletroeletrônicos e uma miríade de mercadorias valiosas posteriormente compradas pelo país exportador. Esse modelo pode estar chegando ao fim...

|

O Setor Mineral Aguarda Medidas Estruturantes

O setor mineral tem contribuído enormemente para o desenvolvimento econômico e social do Brasil. Durante 30 anos (1963-1993), o país conviveu com períodos oscilatórios de estagnação econômica, crises cambiais, déficit na balança de pagamentos e inflação crônica. Ainda assim, no período de 1974 a 1978, a produção mineral aumentou 100%...

|

|

|

|

|

Conselhos ao geólogo recém-formado

Geólogo: sei que muitos estão assustados e desanimados com o cenário difícil que estamos atravessando. Talvez alguns já começam a procurar novos nichos em outras áreas.

Se este é o seu caso leia esta matéria até o fim. Nem tudo está perdido...

|

|

|

Mineração: quem vai tapar os buracos amanhã?

Um dos fantasmas mais assustadores da mineração mundial é o day after, quando a jazida está completamente exaurida e a empresa para de produzir.

É, neste momento, que as autoridades percebem que a maioria das mineradoras não economizou o suficiente para completar um plano de

reabilitação ambiental aceitável...

|

|

|

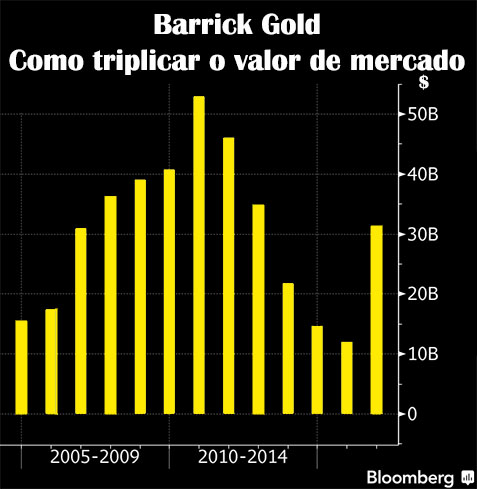

Como a Barrick saiu do buraco e triplicou o seu valor de mercado

Apenas um ano atrás a Barrick vivia a sua pior crise e tinha um valor de mercado pouco maior do que dez bilhões de dólares. Desde então a empresa cortou custos, reduziu o seu AISC, vendeu ativos, pagou parte de sua gigantesca dívida e focou em minas de alto teor: o mais puro exemplo de um gerenciamento de alto nível...

|

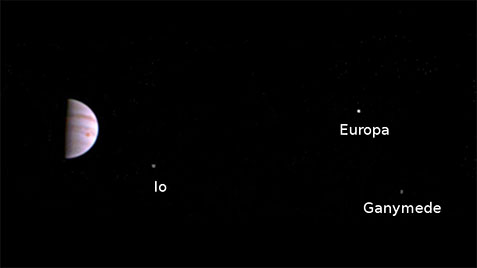

Encontro com Júpiter

Júpiter o maior planeta do sistema solar com uma massa 300 vezes maior do que a da Terra está envolto em mistérios. Com a sua composição de hidrogênio e hélio Júpiter lembra uma estrela que não emite luz.

|

|

|

|

|

Mineração: em quem apostar as fichas?

Após crises de proporções mundiais as grandes empresas de mineração recomeçam a pensar em estratégias globais e investimentos futuros.

Será que o Brasil faz parte deste plano?

|

O dilema da Vale

Como a Vale chegou ao fundo do poço e é obrigada a vender parte dos seus melhores ativos...

|

|

|

|

|

A cleptocracia brasileira

Nunca uma definição se adequou tão bem ao Brasil, um país, completamente controlado por ladrões. Somos, infelizmente, uma cleptocracia madura, evoluída, onde praticamente todos os políticos e seus partidos almejam uma única coisa: roubar, dilapidar, locupletar e permanecer eternamente no poder....

|

Brazil Resources: como comprar muito com tão pouco

A empresa conseguiu, em poucos anos, amealhar um portfólio de mais de 13 milhões de onças de ouro equivalentes comprando, na baixa, aqueles projetos onde outros investiram dezenas de milhões, no período das vacas gordas...

|

|

|

Samarco, um caso mal resolvido

Nem todos concordam com o acordo firmado entre a Samarco, Vale e BHP com o Governo: o MPF recorre contra acordo de R$20 bilhões que prevê a recuperação dos danos causados pela Samarco em 15 anos...

|

|

|

|

|

|

|

|

|

Vale: Murilo Ferreira na mira de Temer

Ferreira substituiu o competente Roger Agnelli em 2011, quando a Vale tinha um valor de mercado gigantesco que ultrapassava a cifra de US$199 bilhões.

Desde então a Vale entrou em parafuso, mesmo quando o preço do minério de ferro ainda subia...

|

|

|

|

|

Geólogo parabéns!

Parabéns à todos os Geólogos que fazem desse planeta um lugar melhor...

|

Não sobra ninguém

Somos todos órfãos de um Brasil sem políticos de qualidade: meros espectadores de roubos planejados entre as paredes do Congresso, onde a única coisa que NÃO interessa é o bem estar da população...

|

Pasadena revisitada: a hora de Dilma Roussef?

Em 2006, quando Dilma Roussef era a Presidente do Conselho de Administração da Petrobras, foi concretizada a compra da Refinaria de Pasadena, no Texas, o primeiro grande rombo da Petrobras: um marco histórico da corrupção brasileira moderna...

|

A corrupção e o empresário brasileiro. Valeu a pena?

Apesar do foco da mídia estar hoje concentrado nas estatais, onde nada se resolve sem a propina e a benção das quadrilhas que tudo controlam, a mesma corrupção grassa em todos os cantos e em todos os segmentos da economia...

|

Simandou: uma ameaça real ao domínio da Vale?

Simandou uma jazida de mais de 2 bilhões de toneladas de minério de ferro de alto teor encravada no coração da Guiné é,

para muitos, o fim do domínio absoluto que a Vale impõe ao setor. Será verdade?

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Assim não dá...

Já em 2013, existiam sinais inequívocos de que o direito de prioridade “incomodava” a vários expoentes do Governo. Não sabíamos o porquê.

Hoje a Lava Jato explicou os motivos...

|

|

|

|

|

|

|

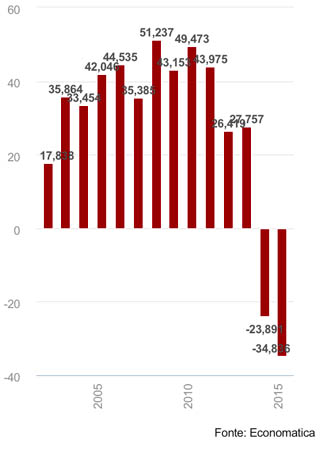

A “dura” vida dos milionários CEOs da mineração

Se você quer ganhar um salário anual de oito dígitos (em dólar) talvez seja interessante considerar a posição de CEO em uma das grandes empresas de mineração como a Rio Tinto, BHP e Vale.

|

|

|

Samarco: quatro meses sem ela

Pela primeira vez, a população defende com vigor a volta da mineradora. Afinal, noventa por cento da arrecadação do município vinha da Samarco...

|